Introduction

Every business wants to be sustainable. Whether you’re an up-and-coming startup or an already established company, saying you don’t want to go bankrupt should be a safe bet. Is there a surefire way to prevent that? Of course not. But there is one thing that is essential if you want to up the chances of your business’ success – a financial model.

Bamboo Group has years of experience in fostering successful startups. And we’re eager to share our knowledge, which is why we wrote this guide for startups big and small. This article will not provide any financial modelling templates (since there’s plenty of those as is), but information on the different elements and technicalities that go into creating a reliable financial model. So let’s get to it, shall we?

Why you need a financial model

What makes financial modelling so important for startups in particular?

It’s common knowledge that the number one reason for startup failure is running out of cash. According to CBInsights, 38% of startups die because of plain old bankruptcy. There are multiple factors that go into either failing to secure the necessary funding or failing to use the funding you did get efficiently. However, the solution to avoiding both of these scenarios is more or less the same: having a good financial model.

But what makes financial modelling so important for startups in particular?

Well, first of all, your company has to be economically viable. The fact of the matter is, you’ll be able to know if your idea can turn into a sustainable business only after you quantify and validate your business plan. Plus, building different versions (“scenarios”) will help you prepare for the future, especially for when things don’t go as planned. When worst comes to worst, you’ll have a safety net in the form of a well-thought-out plan B. At the very least, you’ll be able to anticipate how the worst-case scenario will impact your cash flow, funding, and profitability.

If your startup is seeking investors, having a financial model ready will be a significant advantage. Angel investors, VCs, banks, and subsidy providers will often ask about your financial plan. Having a concrete business plan will help you answer some of their trickier questions, some of which will decide whether or not you’ll get any investments at all. After all, how are you going to raise funding if you haven’t even calculated how much money your company actually needs?

A financial model is necessary to inform both your stakeholders and yourself. How do you know if your business’ outcomes are good if you have no targets or steering information to compare them to? And how will you report your spendings to the stakeholders if you have no benchmarks to set? All this requires forecasting.

Types of financial modelling

How do you get the numbers? What marks your sector’s market size? How much do you spend on marketing and how do you forecast sales?

Building a financial model isn’t exactly difficult. As we’ve mentioned before, there are tons of templates you can find online, and as long as you have someone Excel-savvy around, setting one up won’t be a problem.

The real difficulty lies in the following questions: how do you get the numbers? What marks your sector’s market size? How much do you spend on marketing and how do you forecast sales? All of these and many more can be answered using two different methods: top-down forecasting and bottom-up forecasting.

Top-down forecasting

The top-down method works from a macro/outside-in perspective towards a micro view. First, you take general industry estimates, and then narrow them down into company-specific targets. It essentially helps you make forecasts based on the market share you hope to capture within a certain timeframe.

One model that can help you perform top-down forecasting is TAM SAM SOM. It defines the market size on three different levels:

- the total worldwide market for a product/service (TAM – Total Available Market);

- the part of the market you want to address with your specific offering adjusted for your geographical reach (SAM – Serviceable Available Market);

- the part of the SAM you can realistically capture given the existing competition (SOM – Serviceable Obtainable Market).

The latter (SOM) is equal to your sales target and represents the value of your company’s desired market share.

Let’s imagine you want to set up a pizzeria chain. In that case, the worldwide pizza market is your TAM. If you opened a pizzeria in every single country and also had zero competition, the revenue you generated would be equal to TAM.

But of course, that’s impossible. Let’s start with a more realistic launch in two different cities.

There, you’d have to account for the local demand, which depends on the population size, its food habits, and the revenues generated by pizzerias in similar cities. That’s how you get your SAM – the amount of income you’d earn if you were the only pizzeria in town.

And you’re most likely not. Logically speaking, the majority of your customer base will be the locals living or working near your restaurant, plus a small fraction of people living further away who either happened to be in the area or visited you out of curiosity. All of these customers combined will be your SOM.

So, after you define your targets, you’ll have to estimate all the costs necessary for sales and marketing activities, research and development, general and administrative tasks. Here, you obviously have to aim for profitability within a reasonable timeframe. That is to say, all costs and expenses should not exceed your revenue targets – you need a positive EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization).

The top-down approach has its flaws, namely that it may push you to be way too optimistic with your sales forecasts. A common mistake is calculating SOM with a random market percentage, checking if it’s realistically achievable be damned. A tiny percentage of the market may seem easy enough to capture, but it can still be way too optimistic a year after your company’s launch. To avoid setting those unrealistic goals, you might want to combine the top-down method with the bottom-up approach.

Bottom-up forecasting

Bottom-up forecasting is less dependent on the market, and instead leverages internal company-specific data – sales, internal capacity, etc. The bottom-up approach begins with a micro/inside-out view, building towards a macro view. That way the projection is made based on the factual qualities of your business. For example, a business that’s heavily dependent on online marketing is likely to use such metrics as costs per click, number of website visitors, website visitor conversion rate, etc.

Regardless of your company’s specifics, these measurements will give you a good idea of the business’ potential sales, while taking its budgetary limitations into account. A bottom-up analysis forces you to set realistic goals and makes you consider your resource allocation with more care. Here, you estimate costs, revenues, expenses, and investments in the exact same way – using real company data.

In no small part, the calculations are based on a detailed analysis of the real industry demand for your product. Let’s say you want to sell motorcycle helmets. Those are generally sold in biker stores, so that’s what you have to analyze first and foremost.

Check how many motorcycle stores there are in your country. For the sake of an example, let’s use the US: there are approximately 7000 motorcycle stores across the entire country. Naturally, not all of them will want to stock your helmets, and in reality, you will likely be able to secure a deal with maybe 10-15% of them. Here, for the sake of simplicity, we’ll use 10%.

So your helmets will be stocked in 700 stores across the US. The next question is, “How many helmets does a biker shop sell in a year?” Now, this number will vary from store to store, but let’s imagine that the ones you’ve talked to sell 100 helmets a year on average. And let’s be frank: those 100 helmets won’t be yours. Not all of them, at least.

We can settle for a modest 10 helmets a shop. In that case, you’ll be selling approximately 10 times 700 helmets every year – that’s 7000 motorcycle helmets sold yearly. A modest result, but one that is as realistic as it gets.

And here’s where the main flaw of this method becomes apparent: it’s not just time-consuming when it comes to collecting all the necessary market data, but the results of its calculations can be plain discouraging.

When you’re a startup, optimism is important for keeping the spirits high – but that’s not all there is to it. A more optimistic prognosis can help you convince others of your startup’s potential, thus securing the necessary funding. Investors want their startups to grow fast, and a bottom-up approach might not reflect that.

When every sale has to be rationalized with its point of departure being the maximum capacity of your company, creating a forecast with a steep growth curve becomes quite difficult. The bottom-up approach doesn’t take such factors as word-of-mouth and virality into account; it also doesn’t account for the growth boost that investments will bring to the company.

In view of that, it’s better to build forecasts using a combination of these two approaches, especially if you rely on external funding for fast growth. The bottom-up approach works best for short-term forecasts (1-2 years ahead), while top-down forecasting is good for longer-term predictions (3-5 years ahead). When talking to investors, this will help you substantiate and defend your short-term targets, as well as demonstrate the much-desired ambition with your long-term goals.

Startup financial model inputs

Let’s start with the obvious: you need a certain input to produce a certain output. In other words, you need to enter certain numbers into the financial model in order for it to produce useful results.

There are 6 main elements that serve as the input sheets of a financial model. Though, technically there are 7, the seventh one being “settings”. These define the general characteristics of the model, including its forecasting period, the currency used, possible taxes, etc.

Before we go into each of the 6 elements separately, keep in mind that a financial model is essentially a reflection of your business strategy, model, or vision. In a way, your financial model and your business model canvas are reflections of each other. So if you’re ever conflicted about which elements to include in your financial model, your business model canvas can serve as a valuable guide for deciding on your financial plan.

Revenue

The first input sheet is the revenue forecast. This one can be tricky, especially if you haven’t archived any of your past sales yet. Still, it should be manageable if you follow the directions below.

Revenue forecasts are usually made using a combination of top-down and bottom-up methods. As we’ve already mentioned, the bottom-up method works best for short-term sales forecasts (1-2 years ahead), while top-down forecasts are more suitable for longer-term predictions (3-5 years ahead). That way you get to both substantiate your short-term targets and demonstrate your long-term potential to the investor.

If you’re having trouble estimating the demand for your product, try doing some search query research. There’s a variety of keyword tools (KWFinder, Google Keyword Planner, Semrush, etc.) that give you insights into how popular certain words and phrases are in search engines and the demand for the goods and services you’re trying to sell.

Purchase intent plays a big role here. Not all keywords are created equal, and some are more likely to signify that a customer wants to buy your product. There are three main types of search queries: navigational (“paypal”), informational (“financial software”), and transactional (“buy financial software”). Transactional queries demonstrate the actual demand for your product, so they are the ones you really want to keep an eye on.

You can also limit your search volumes by city, country, continent, or the world as a whole to get a more detailed perspective.

Now that you got the gist of how forecasting works, here’s how you write that forecast of yours down:

- List all the services and products you are selling;

- Determine the units for measuring your sales (i.e. a soft drink company can measure its sales in bottles, cans, liters, gallons, etc.);

- Forecast the number of units sold per sales unit (based on the top-down and bottom-up analyses);

- Add selling prices.

The way your revenue forecast is constructed depends on the business model you’re using. For example, SaaS businesses usually build their revenue forecasts on such metrics as existing customers, new customers, and customer churn. Really, you can look up a suitable financial model template on the web or book an expert consultation to determine what model would fit your startup best.

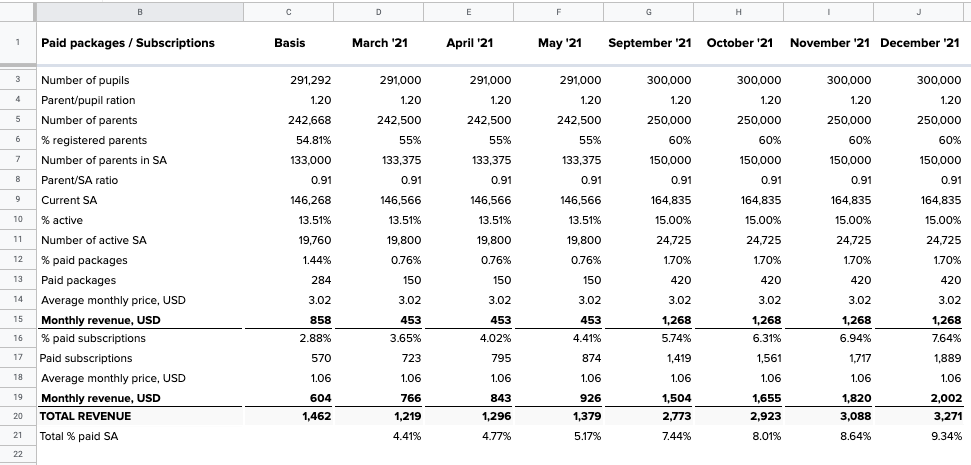

Let’s say your startup is developing an EdTech application for schools, students, and their parents. You get revenue from selling premium packages to parents. In that case, your task is to forecast the total revenue while accounting for the increase in the number of packages/subscriptions sold.

Here’s what your calculations may look like:

COGS

COGS, or Cost Of Goods Sold (a.k.a. Cost Of Sales and Cost Of Revenue), is the sum of all costs that are necessary for the company to create its products or deliver services. These costs are absolute – without them, the product or service cannot exist.

COGS depends on what your company is selling. If your business produces tangible goods, COGS includes the price of the required production materials. If your business deals in, say, consultancy, your COGS will mainly consist of personnel costs. Let’s use a SaaS business as an example once again: its COGS will include hosting costs, onboarding costs, online payment costs, and customer support.

But how does one forecast COGS?

One way to do that is to look at the sales targets defined in the revenue forecast. If you’re selling a tangible product, you can clearly see how many units you need to sell within a particular time period. So, what you do is combine labor costs and the costs of raw materials per sales unit.

You have to precisely know all the costs involved. Let’s say your company produces pencils. In that case, you have to know how many grams of wood is needed to produce one pencil and how many grams of graphite is needed to make one pencil lead. You also need to know how much a kilo of wood costs and how much a kilo of graphite goes for.

Multiply those numbers by the number of units you need to sell and add the salaries of the employees involved in the production. That’s pretty much it!

However, COGS also depends on your company’s business model. Sometimes it’s better to forecast COGS using totals (totals per month, for example). And sometimes COGS can be a percentage of your revenues (for instance, if you work with sales commissions).

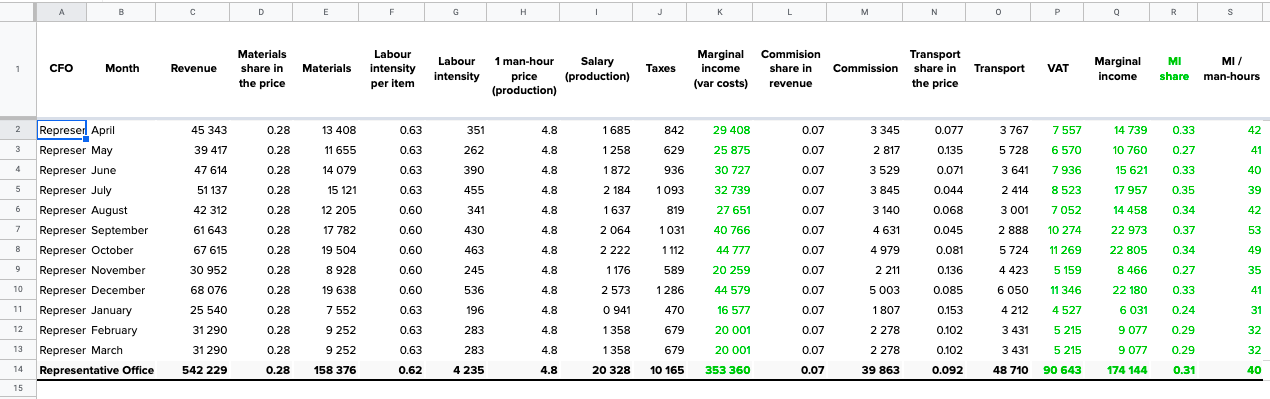

The following table illustrates the influence of COGS (Materials, Salary, and Taxes) on the marginal income, as well as shows their share in the price that demonstrates the significance of any given item:

As a whole, the table accounts for direct variable costs (with transport costs being semi-direct). It makes planning and modelling the item cost easier whenever the sales, salary, tax, or any other kind of % changes. The bigger the item’s share, the more attention that item requires, since any change to its % will have a greater effect.

The table also helps understand the level of variable costs combined with fixed costs, which aids in calculating the break-even point.

OPEX

OPEX (a.k.a. Operating Expenses) are the costs a business accumulates as it performs its basic operations. Unlike COGS, they’re not necessary for goods production and/or services delivery, but include both the manufacturing overhead and expenses related to supporting various operating activities – sales, marketing, research, development, general administrative tasks, and so on.

In general, a startup’s OPEX include:

- depreciation;

- amortization;

- rent;

- repair works;

- travelling;

- events;

- legal costs;

- accounting;

- utilities;

- insurance;

- promotional materials;

- online marketing;

- prototyping;

- patent costs;

- IT costs (e. g. subscription fees for using certain software);

- office supplies;

- payroll costs (for employees not part of COGS);

- others.

But you can’t always predict your expenses in the long term. Thus, it’s good to save a certain percentage of your revenues for different expense categories (e. g. dedicate 10% of your yearly revenue to sales and marketing).

The most important part of this is having your operating expenses align with your corporate strategy. The more your business relies on a certain activity (for example, online marketing), the more resources should be allocated to it.

Your OPEX may include sections similar to these:

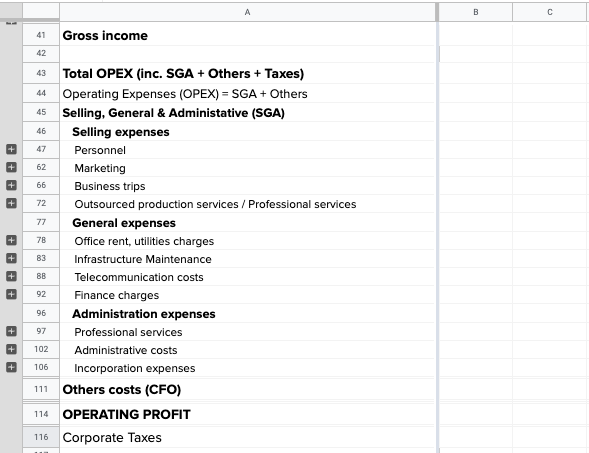

The first table shows a detailed breakdown of a company’s OPEX in financial documentation. The OPEX are classified as selling, general, and administrative expenses.

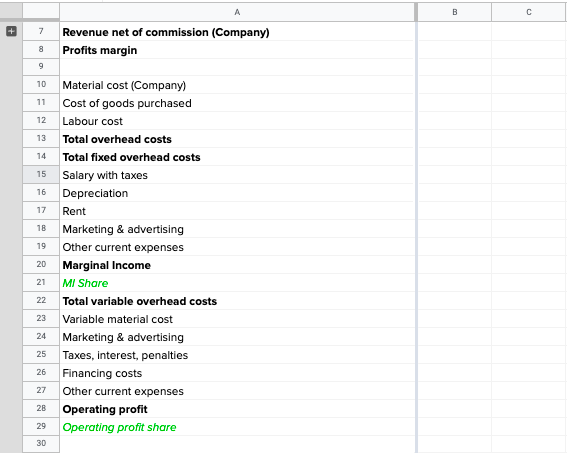

The second table allows you to see the impact discounts make on product sales, as well as shows the link between direct cost variables and the labour costs, commission revenue (when working with dealers), sales personnel commission (when the bonus is linked to the revenue), etc.

To get your budget, enter the % and get the absolute revenue and cost numbers. When doing actual accounting enter the actual for the revenue and costs to get the actual % of variable costs. If you compare the budget and actual percentages, you’ll be able to objectively judge the effectiveness of the business, track market trends, and point out when and how to change your business processes.

This table is a part of financial documentation that accounts for fixed and variable overhead costs when calculating the profits margin and the operating profit.

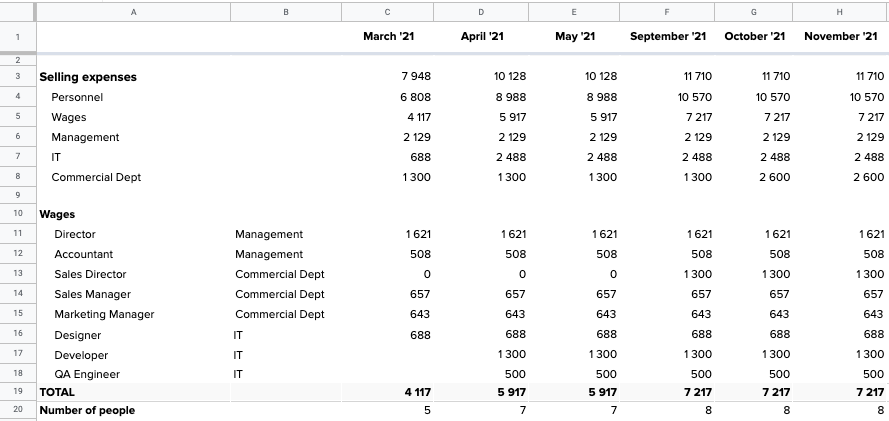

Staff

Staff forecasting is one of the easiest. It implies projecting the number of employees hired and their respective salaries, benefits, and payroll taxes. One method to simplify staff forecasting is by splitting up your personnel into different categories.

For example:

- Direct labor. These employees are directly engaged with the production of your goods or services. For example, if you deal in hardware, these will be engineers and technicians, and if your company does consulting, these will be junior advisors. Naturally, the costs of these employees are part of COGS.

- Sales and marketing. These include sales managers, marketing specialists, social media managers, copywriters, etc. The costs of this and all the following personnel categories are part of OPEX.

- Research and development. This category includes R&D managers, technicians, software engineers (if the company deals in software), project managers, account managers, business analysts, rank and files specialists.

- General administration. This includes C-level and back office personnel, that is the CEO, CFO, CMO, or accountants, secretaries, and others.

In the end, your staff forecast may look something like this:

To check how realistic your predictions are, you can divide your projected yearly revenue by the number of employees (or FTEs – Full-Time Equivalents) projected for that year. This will show how much revenue one employee is expected to generate and provide a basis for comparison with your industry competitors. If your revenue per employee is over 500K USD only a couple of years after launch, your forecast is probably way too optimistic.

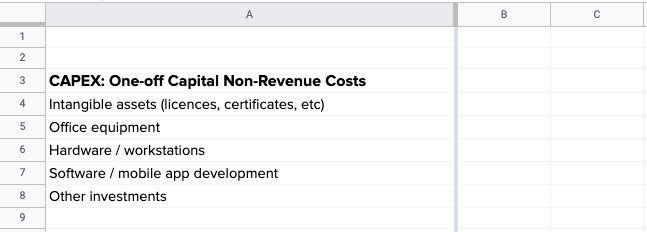

CAPEX – Capital expenditures

Capital expenditures, or investments in assets, are the funds used to acquire or upgrade the company’s physical assets (physical property, intellectual property, buildings, equipment). These expenditures help either maintain or expand the scope of your business’ operations, including everything from repairing a leaky office roof to building a new factory.

Capital expenditures usually depend on the industry a business operates in and the kind of services it provides. Startups tend to invest in computers, software, machinery, and offices.

One thing startups are often advised to do is categorize their expenses as capital expenditures instead of operating expenses. The thing is, all payments related to investments in assets are written as profit and loss statements spread out over several years due to accounting technicalities. Because of that, they do not show up all at once in the year of purchase and have a less visible impact on your profits. But careful with the rules: they’re pretty strict about what does and does not qualify as assets.

Also remember that while capitalized costs may be a reflection of your actual processes (when the payroll of your engineers is added to your IP’s value, for example), investors may see them as a cheap trick during the process of compliance.

Here’s what your CAPEX might look like:

Financing

The final input sheet is a financial module. The financial sheet features several streams: equity, loans, convertible notes, and subsidies. Its main goal is to check how your company’s funding needs change whenever you add different types of funding to the model.

Before we go into these types, it’s good to mention that young startups tend to think that entrepreneurship is a cash-out kind of deal only upon immediate success. In reality, cash-in is a much more applicable and accessible option. With that in mind, let’s look at the different kinds of financing startups can apply for.

Equity financing is raised from angel investors or VCs, which act as shareholders. This means that equity investments equal you losing some control of the business: stakeholders don’t just receive part of your company’s profits, they can take part in managing it, too.

That said, equity funding is the most common type of financing for startups. Why? Because loans can be exceedingly hard to get as a young business. Banks are especially cautious when it comes to giving out loans, and startups often struggle to meet the criteria in terms of revenue generation.

Still, if your company does manage to secure a loan, it comes with its share of advantages. First of all, your business does not gain a new owner – it’s all yours. Secondly, interest can be conveniently deducted from your tax. Finally, debt can act as a stimulus for your team to be more efficient with using resources and building revenue.

One option that’s considered good for startups in particular is a convertible note. Convertible notes are short-term debts that startups don’t have to repay with interest. Instead, investors get their money back through shares of preferred stock.

One of this method’s key advantages is that it pushes startup valuation further down the road, that is, until the company’s first major round of financing. This means that valuing the startup will be a lot easier, since there will be a lot more data points to base the calculations on.

One of the key advantages of issuing convertible notes is that the valuation issue is kicked down the road until the Series A round of financing – when there are a lot more data points and thus it’s much easier to value the startup (i.e., price the round).

A convertible note is a short-term debt that converts into equity. In the context of seed financing, the debt typically automatically converts into shares of preferred stock upon the closing of a Series A round of financing. In other words, investors loan money to a startup as its first round of funding; and then rather than get their money back with interest, the investors receive shares of preferred stock as part of the startup’s initial preferred stock financing, based on the terms of the note.

Finally, subsidies are monetary grants provided by either the government, a company, or an individual to help a startup develop faster. These are essentially gifts, which you do not need to repay. Still, that doesn’t mean you can waste them without a second thought. They’re just as important as any other financial resource, and should be treated accordingly – that is, with care.

Other startup financial model elements

Some of the startup financial model elements we’ve described need additional tweaking before you get usable outputs out of them. That tweaking is done with the help of several supporting schemes. Let’s take a closer look at each of these schemes.

Working capital

Firstly, let’s define what working capital is. Working capital is the difference between your current assets and current liabilities on the balance sheet. In other words, it’s the difference between the amount of money paid by clients vs. the amount of money due for all sorts of corporate expenses.

The difference is calculated at a certain date, when the amount of money the startup has earned and the amount of money it has to pay to employees, investors, сontractors, the tax office, and others are more or less set in stone.

It is incredibly important that the company is able to make all the payments in time even if its earnings arrive later than what was initially expected. One of the metrics of a company’s solvency is the cash ratio – the sum of the company’s cash and cash equivalents divided by its current liabilities. Ideally, the ratio should exceed 1.

Timing the payments from clients starts simple, but gets more difficult as your business expands. Fast company growth may mean that your customer count is spiking, but when their payments come with a delay, even a gross margin positive customer can drain cash for a while.

This issue is further aggravated if your startup works with purchase orders, as a purchase order system can delay payments for as long as several months. And if you have different enterprise clients requesting different invoices or purchase orders, payments can take an even longer time to show up (though startups that use a subscription model mitigate that issue, as they can get large sums of money upfront).

Some may try to stretch out their bill payments, as it will have a temporary positive impact on the company’s cash flow. However, it’s a high-effort maneuver and will very likely annoy your vendors so much that they stop doing any business with your startup. So it’s definitely not the best financial strategy.

Generally speaking, you’ll be able to make better financial projections – and, consequently, better financial decisions – if you introduce a cash-flow management process into your daily routine and think through your company’s working capital.

Depreciation and amortization

Depreciation is something that occurs when an economic asset is used up. The fact of the matter is, assets degrade and lose value as they are being used, and different assets lose value at different rates. A so-called depreciation schedule helps calculate those differences.

A basic depreciation schedule lists different asset classes, the kind of depreciation they go through, and the cumulative depreciation they’ve accumulated at various points in time. If properly maintained, the schedule will give you a good idea of how many resources you still have in store, as well as of their current value.

While depreciation refers to the decline in the value of tangible assets as they’re used up, amortization is the decline in the value of intangible assets over their lifespan. These include patents, trademarks, brand value, lease rental agreements, and so on.

Say, you have a 20-year patent on a piece of technology. Since you spent $20,000 on designing and building the technology, that’s what the initial cost of the patent is. Amortization is calculated using the following formula:

(Initial Value – Residual Value) / Lifespan = Amortization Expense

Therefore, your yearly amortization expense will be $1,000, that is $20,000 / 20 years.

Taxes

This one is pretty self-explanatory. Every registered startup has to annually account for tax via a tax return. If your business has a taxable net income, taxes are deducted from your total in the profit and loss statement. Alternatively, you can carry your losses forward to reduce the amount of tax you’ll need to pay in the future. In that case you’ll need to add a separate carryforward scheme to your financial model.

Different countries provide different conditions for startups, so some end up being more startup-friendly than others. For example, Estonia is considered a startup-friendly country due to the significant support given to businesses. This means lower OPEX, great tax benefits, and tax holidays.

Discounted Cash Flow

Discounted Cash Flow, or DCF, is a valuation method commonly used to determine whether a company is worth investing in or not. It basically goes as follows:

- create financial projections for your company;

- determine the projected free cash flows;

- determine the discount factor;

- use the discount factor to calculate the terminal value and the net present value of your free cash flows;

- sum up the results.

This method’s biggest advantage is that it values your startup based on its future performance. It’s especially useful for pre-seed startups, because lots of them have not generated any revenue yet, but need to secure their investor’s trust.

On the other hand, DCF’s greatest disadvantage is that it’s merely a formula. It is therefore very sensitive to the variables you input. So, the accuracy of DCF is heavily dependent on how accurate your own predictions of the company’s future performance are.

Startup financial model outputs

Looking at financial statements, operational cash flow, and KPIs in detail.

So, you’ve inputted all the necessary information into the financial model. What do you get out of it?

Really, it depends on your startup. Every industry and company is different. Everyone has their own interests and prioritizes different metrics. It is therefore fair to say that every financial model has its specific characteristics and, therefore, its specific outputs. That said, any decent financial model needs to contain:

- financial statements;

- operational cash flow;

- KPI.

Let’s look at each of them in more detail.

Financial statements

A good financial model has to include forecasts of the three financial statements:

- the profit and loss statement – P&L;

- the balance sheet – BS;

- the cash flow statement – CF.

These statements are the generally accepted way of communicating financial data across banks, companies, investors, governments, or really anyone that needs to demonstrate their financial performance. Every financial professional is capable of interpreting financial statements, so it’s crucial to have a forecast based on them when your startup is raising funds.

The P&L statement is an overview of all the income and expenses generated by your company within a certain period of time. Basically, it shows how profitable your business is.

It consists of several performance indicators: gross margin, EBITDA (deciphered above), and net margin. EBITDA is particularly important to investors, because it gives insight into the company’s performance; they can clearly see how your startup fares in comparison to other businesses. What’s more, the P&L can be used to compare different time periods, budget vs actual performance, and many other metrics.

All of the company’s assets and liabilities can be reflected in a balance sheet (BS). It represents a specific point in time (the end of the year, for example) instead of an entire time period like the P&L.

Assets show how the company uses its funds. Assets fall into a variety of categories: they can be current and noncurrent, tangible and intangible, financial (i.e. the money used to pay for inventory) and physical (computers, buildings, etc.).

Liabilities, on the other hand, show the obligations the company has and how it has financed itself through debt. The difference between the value of assets and liabilities consists of the paid-in capital from investors that finance the assets not covered by debt, a. k. a. equity. So essentially, assets are a sum of equity and liabilities.

This is what makes the balance sheet, well, “balanced”. The value of the company is represented by shareholders’ equity – that is, the amount of money the shareholders would get if all the business’ assets were liquidated and debts repaid.

Finally, the cash flow statement (CF) shows all of the money going in and out of the company over a specific period of time. It includes: the operating cash flow, the investment cash flow, and the financial cash flow.

Operating cash flow reflects cash inflows and outflows from the startup’s core business operations.

Investment cash flow represents the changes in asset and equipment-related investments. It will usually have an outflow (investing in assets costs money, after all), but it can also be positive if the company is selling its assets (real estate, for instance).

Financial cash flow shows the effects of different financing activities. Cash inflow happens when the company raises its capital through either loans or equity, and cash outflow occurs from paying dividends or interests.

Basically, the CF allows you to make informed decisions on your operations and helps avoid or monitor company debt. It also helps define your business’ investment strategy.

KPI

A startup’s financial model typically includes some company- or sector-specific KPIs – key performance indicators. These serve as crucial metrics for your business’ performance, which makes them equally interesting to company owners and investors.

KPIs also allow you to experiment with different acquisition strategies, business models, and cost structures. When used well, KPIs can seriously boost your team’s success by directing their efforts in the right direction.

Some KPIs show sales and profitability performance (revenue growth rate, EBITDA margin, gross margin, etc.), some are related to cash flow and increasing investments (burn rate, runway, funding need), and some are based on company and industry-specific metrics. SaaS businesses, for example, estimate the LTV – customer lifetime value, CAC – customer acquisition costs, the LTV/CAC ratio, and customer churn rate. Research what metrics are important in your company’s industry and include them in your financial model.

The notion of unit economics is closely related to KPIs. What unit economics do is simplify the process of managing and calculating all the different key metrics. Basically, they measure profitability on a per unit basis and answer the question, “Can the profit you make from a single unit (customer) exceed the costs of acquiring it?”.

Operating cash flow

A forecast of the three financial statements is generally shown on a yearly basis for fundraising purposes. And since early-stage startups are more focused on showing their long-term growth potential, monthly overviews aren’t really needed.

Still, your financial model should include an operating cash flow for the coming year. It will help with your daily financial management, as it addresses the questions that yearly financial statements cannot answer, such as the timing of cash inflows and outflows. Plus, it provides an opportunity to track your actual performance and compare it to expected monthly budgets. This will help you cut costs and anticipate potential cash dips months in advance.

Building an operating cash flow is simple: list all the categories of inflows and outflows, add a starting balance, and see what’s left at the end of each month. All this can be easily done in Excel.

Some extra precautions

At last, your financial model is complete, and you’ve seemingly got some solid outputs from it. Great! But don’t think that you’re done just yet. There are a couple of extra measures you need to make in order to ensure the model’s effectiveness and sustainability.

Sanity check

It’s always best to double check your calculations. A sanity check will help you ensure that your financial model is functional and isn’t subject to common startup pitfalls. As obvious as these mistakes may seem, they are called common for a reason, so this little step is not one you want to skip.

The first batch of mistakes stems from being either too optimistic about revenue projections. Overconfidence kills even good undertakings! This can reach ridiculous levels, when the most ambitious revenue projections extend past the real market size. That excessive optimism may also lead to you underestimating the number (and costs) of employees needed to grow your business.

Similarly, being too confident in your finances can lead to brushing off the importance of the working capital – that is, completely disregarding the time it will take for you to get usable sums of money. Some operational expenses can also be left out, which is why it’s always better to ensure that they align with your forecasted revenues and strategy.

Speaking of strategy, a weirdly common mistake is the financial model being in conflict with the company’s business plan. This one is easily preventable, however: as long as you take care to reference the overall business strategy when constructing the model, this pitfall is unlikely to affect you.

Finally, make sure that your funding is adequately explained and your assumptions are clearly defined. A detailed cost breakdown and proper proof for the numbers you have written down will not only help you get a clearer idea of how to manage your future resources, but make you a more trustworthy partner to investors.

One thing investors also value is a realistic view of the gross, EBITDA, and net margins. Therefore, you have to be ready to answer their questions regarding both your current and forecasted margins. This will further solidify your startup as a reliable prospective business and aid you in building an effective financial plan.

Multiple case scenarios

Luck is a tricky thing, and it’s naive to assume that it will be on your business’ side every step of the way. Your launch may get postponed for months, the expenses may turn out to be double than what you expected, and the product sales may be lower than what you thought they’d be. And having a backup plan that accounts for such sub-optimal possibilities is a must.

This is why it’s better to create not one, but three possible scenarios for a financial model. The base case scenario is the most grounded of the bunch, outlining your company’s default course of action. As we’ve already said, however, there’s no guarantee of it being completely feasible. Therefore, a worst case scenario is a very important thing to have in store in case the base prognosis turns out to be a little too optimistic.

But of course, it’s not all doom and gloom. The third case scenario is just as important to have as the other two – that is, a best case scenario. As the name suggests, it’s supposed to account for the possibility of things going better than you expected – more sales, bigger investments, faster growth. While making a best case scenario may not seem as dire as having the base and the worst case ones prepared, it will help your company leverage the benefits of an unexpected success a lot more efficiently than it would have otherwise.

Validating the numbers

Regardless of which approach you use, you have to be able to substantiate your numbers with assumptions. Being a startup, you may not always have the needed historic data to use as a reference. However, you’ll still need to present some proof for the results of your calculations. Investors are typically interested in the reasoning behind your numbers. No one wants to put money into a disorganized venture, let alone a scam.

But what are “assumptions”? Anything that validates your numbers, really – market research, historic sales, conversion rates, website traffic, search volume, current multiples, and so on. You can store evidence like that in a designated place (a Drive folder, for example) and slowly build a substantial library to underpin all of your calculations.

If you’ve done all of the above, congratulations! You now have a fully functional, foolproof financial model – one that you’ll be able to rely on in making important management decisions, and one you’ll be able to confidently showcase to your investors.

To sum it all up

If we were to sum up the most common mistakes in startup financial modelling, they’d be as follows:

- Not having a coordinated project team. It’s important that everyone understands the processes involved, and knows the value of said processes. A good financial model is balanced in its complexity – it’s neither too shallow, nor too convoluted. Therefore, it should be easy enough to understand for everyone involved.

- The financial model conflicts the business model. The two must reflect each other in order to function properly. The right thing to do is to use a financial model as a basis for building your business model, as well as to have the ability to analyze the factual and forecast plans.

- Using incorrect source data. Sometimes administrative accounting and financial accounting are extremely different, which is why it’s crucial to double check which metrics you’re using for calculations.

- Not accounting for all the expenses involved. A financial model doesn’t just contain operational expenses, but also marketing research and new technology implementation costs.

- Incorrect calculation of сash flows (operational, investment, financial), not accounting for cash gaps. One must pay particular attention to the working capital, product turnover, and all possible payment delays.

- Subjective discount rate evaluation. Look at all the aspects of financing – things like certain national specifics, funding shares, and funding costs really do matter.

- Excessive optimism. Optimism is great when you’re presenting your business to investors – enthusiasm is contagious, after all. That said, having a plan B is paramount in case things don’t go exactly as planned. So it’s important that your model accounts for multiple possible scenarios.

- No project risk analysis. There are no risk-free projects. You have to be prepared to combat the challenges that may arise in the process, and analyzing all possible pitfalls is the best way to do so. There are several risk analysis methods:

- analyzing the effect of different factors or analyzing the project’s susceptibility to change;

- analyzing different scenarios or analyzing the effect of a combination of different factors;

- imitation modelling (the Monte Carlo method).

At the very least you need to compare all the scenarios that you have laid out. Find out what affects your revenue and other metrics the most. Set up your control points (each control point standing for the metric you want to analyze) and go through them one by one. This will help you define the most prominent factors at play and to devise ways of avoiding unpleasant outcomes.

If you pay attention to the abovementioned factors, you’re far more likely to construct a fully functional, well thought out financial model that will help your business grow while generating a consistent stream of revenue.

Conclusion

Of course, you can also come up with whatever numbers you want. But what’s the point?

Financial modelling is integral for any business that wants to last. It helps prepare your company for a variety of possible scenarios and serves as an amazing planning tool. Financial models also help startups secure investments, demonstrating your company’s ambition, professionalism, and reliability.

Of course, you can also come up with whatever numbers you want. But what’s the point? Just to get initial financing and then completely forget about your promises? In that case, you will simply waste everyone’s time and money. The investor will want to see results, and is likely to stop financing you or demand a refund if you fail to meet their expectations.

Tricking won’t do you any good. So just be honest about your forecasts and stay positive – to a reasonable extent, that is.

We hope you found this guide to financial modelling for startups helpful. If you still have some questions you would like to ask, feel free to reach out. Being a company with years of expertise in nurturing startups, Bamboo Group will be happy to consult you on the best business practices and development strategies. Thank you for your attention, and best of luck with your business ventures!